February 19, 2016

But the rial has only strengthened marginally, and, in fact, is only back to where it was last October, after the nuclear deal was agreed to.

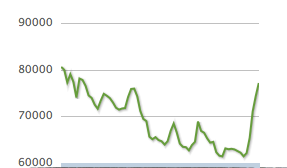

The main index of the Tehran Stock Exchange (TSE) has soared 26 percent since its recent low of 61,414 on December 22. That is a huge increase in less than two months.

It stood at 77,378 Monday. But it must be noted that it remains 14 percent below its record high of 89,501, set just over two years ago on January 5, 2014. And since those intervening two years saw inflation on the order of 25 percent, the index will need to surpass 112,000 before one can talk of real growth instead of paper growth.

But that can’t detract from the fact that Iranian investors are returning to the stock market with enthusiasm. Average daily trading turnover has tripled from last year to around $150 million.

The economy is still struggling—growth is close to zero, though expected to rise; the jobless rate exceeds 10 percent; many banks face mountains of bad debt; and inflation remains among the highest in the world after falling from more than 40 percent to just a hair under 10 percent.

As a result, some commentators are cautioning that the notoriously volatile stock market may not hold on to its gains.

“The Tehran bourse is disregarding warnings and the condition of world markets…. It is going down the same road as in 2015, the result of which will only be a lack of confidence and the flight of capital from this market,” the conservative Nassim news agency said in a pessimistic commentary last week.

But many investors are clearly betting that by restoring Iran’s links with the rest of the world and attracting foreign capital and technology, the end of sanctions will trigger a long-term economic boom.

“The actual benefits of the lifting of sanctions will take six to 12 months to start to feed into companies’ financials,” Payam Malayeri, head of asset management at Tehran-based Griffon Capital, told the Reuters news agency. “Investors are … looking ahead to corporate earnings growth in 2017 and 2018.”

So far, auto stocks have led the stock market rally because of prospects for tie-ups with foreign firms; Iran Khodro, which announced a 50/50 venture to build cars with Peugeot, has rocketed 52 percent. Pharmaceutical and engineering shares have also surged; banks and petrochemicals have under-performed.

Almost all new buying of stocks has been by local retail investors. Foreigners still invest next-to-nothing in Iranian stocks.

Ramin Rabii, chief executive of Iranian investment group Turquoise Partners, which manages most foreign portfolio investment on the Tehran exchange, estimated $10 million to 20 million had entered in the past three months, bringing the total outstanding near $100 million.

“We may see $100 to $200 million of fresh foreign money in the next 12 months,” Rabii said. That would still be minuscule—not even one-third of 1 percent—compared to the market’s capitalization, equivalent to $94 billion at the free market exchange rate.

Some companies or sectors could actually suffer as the lifting of sanctions exposes them to more competition. Renaissance Capital says steel producers’ profit margins may shrink as imports of cheap metal increase.

Another risk is that reforms to improve the business climate could be stalled by political feuding.

But Reuters says some powerful factors support the bourse’s uptrend. For example, under many ways of valuing stocks, Iranian equities are still cheap by international standards. The market is trading at 7.0-to-7.5 times this year’s projected corporate earnings—above its long-term average of 6 times, but well below 11 times, the average for the world’s frontier markets, Rabii said.

Meanwhile, falling interest rates on bank deposits could push billions of dollars into stocks, Malayeri said. Deposit rates soared in the sanctions era; authorities have begun guiding them down from above 20 percent.

Rabii said inefficiencies and distortions of the sanctions era had left pockets of value in the stock market that both local and foreign investors would exploit in coming years.

“You could buy a cement plant by acquiring a company for a third of the cost of building one from scratch,” he said. “This is the kind of thing that will attract foreign investment.”